UK Online Slots GGY Climbs 10% to £788 Million in Q3 2025/26 as Spins Hit New Highs, Gambling Commission Figures Show

UK Online Slots GGY Climbs 10% to £788 Million in Q3 2025/26 as Spins Hit New Highs, Gambling Commission Figures Show

The Latest Snapshot from the Gambling Commission

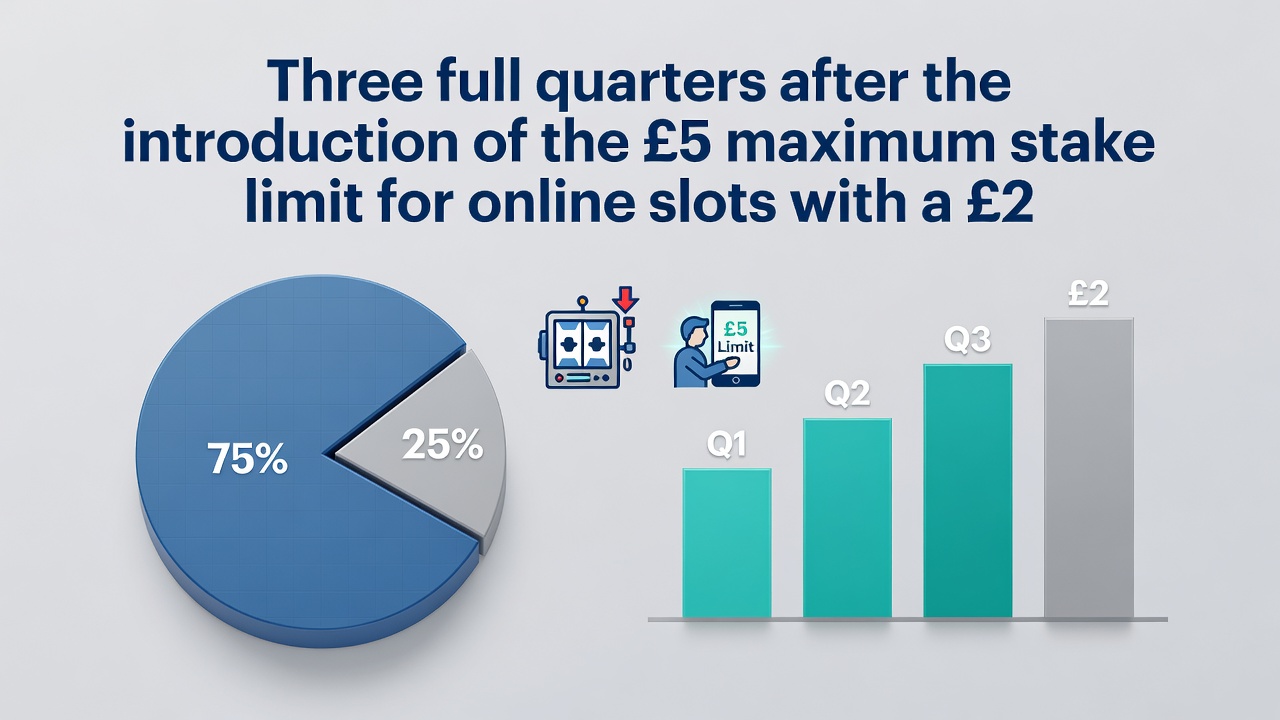

Recent data from the UK Gambling Commission, released in February 2026 and covering the third quarter of the 2025/26 financial year from October to December 2025, reveals notable shifts in online slots activity; Gross Gambling Yield (GGY) for these games rose 10% year-on-year to £788 million, while total spins increased by 7% to a staggering 25.7 billion, marking the third straight quarter of record highs since online slots stake limits came into effect back in 2023.

Observers note how these figures, drawn from the largest online operators who account for roughly 70% of the market, paint a picture of sustained engagement despite regulatory changes aimed at curbing potential harms; average monthly active accounts climbed 5% to 4.6 million, yet session lengths dipped by 2 minutes on average to 16 minutes per session, and those exceeding one hour dropped sharply by 16% to 8.9 million, representing just 4.4% of all sessions during the period.

What's interesting here is the contrast between rising volumes and shortening play times, a trend that experts tracking gambling behaviors have flagged as potentially reflective of broader player adaptations to the new landscape; the data, published just weeks ago as of March 2026, underscores how the industry navigates these limits while activity metrics continue to push upward.

Breaking Down the Core Metrics

GGY, essentially the net revenue from gambling after player winnings but before operator costs, hit that £788 million mark for online slots alone in Q3, up from the previous year's equivalent period; spins, meanwhile, totaled 25.7 billion across the covered operators, a 7% jump that signals players aren't dialing back on the sheer number of plays despite caps on individual stakes introduced to protect vulnerable participants.

And here's where it gets detailed: those stake limits, set at £5 per spin for players aged 25 and over and £2 for under-25s since their rollout, haven't dampened overall participation; active accounts averaged 4.6 million monthly, growing 5% year-on-year, which means more people are logging in regularly, spinning more frequently in aggregate, even as individual sessions compress.

Session data tells its own story, with average lengths falling to 16 minutes from 18, a shift that researchers attribute to quicker play patterns or perhaps heightened awareness of time spent; longer hauls over 60 minutes, often a red flag for potential problem gambling, plummeted to 8.9 million instances, down 16%, now making up only 4.4% of total sessions compared to higher shares before.

- GGY: +10% to £788m

- Spins: +7% to 25.7bn

- Active accounts: +5% to 4.6m monthly average

- Avg session length: -2 min to 16 min

- Sessions >1hr: -16% to 8.9m (4.4% of total)

Take one analyst who pored over similar quarterly releases; they pointed out how these peaks in spins and GGY, the third in a row post-limits, suggest operators have adjusted offerings effectively, perhaps through lower-stake games or promotional spins that keep volumes high without breaching rules.

Stake Limits in Context: Third Quarter of Peaks

Since the online slots stake limits landed in late 2023, each of the past three quarters has delivered fresh records on spins and GGY for the biggest players in the space; Q3 2025/26 continues that streak, with data indicating the measures haven't slowed the market's momentum, at least in terms of top-line activity metrics.

But here's the thing: while yields and spins climb, the drop in prolonged sessions hints at behavioral nudges working as intended; experts who've studied pre- and post-limit data observe fewer marathon plays, which aligns with the Commission's goals of reducing exposure risks, even as overall engagement holds steady or grows.

The reality is these limits apply specifically to online slots on domestic sites targeting UK players, leaving room for innovation like feature buys or free spin mechanics that don't count toward stake caps; operators covered in the report, representing that 70% market slice, demonstrate resilience, with GGY growth outpacing spins growth slightly, pointing to healthier margins per play.

Player Engagement Patterns Shift

Average monthly active accounts reaching 4.6 million reflects broader accessibility or appeal, up 5% from last year, yet the 2-minute trim in session duration to 16 minutes suggests quicker, more episodic play; those extended sessions over an hour, now a mere 4.4% slice, fell to 8.9 million, a 16% decline that observers link directly to limit-induced efficiencies.

Turns out, people often find themselves dipping in for short bursts rather than settling in for hours, a pattern echoed in prior Commission releases; one study of operator-submitted data revealed similar trends across demographics, where younger players under stake limits adapt fastest, spinning more but stopping sooner.

So, with 25.7 billion spins fueling £788 million in GGY, the math checks out on intensified but brief interactions; that's where the rubber meets the road for regulators monitoring if volume spikes mask underlying risks, though current figures show positive signals on session controls.

Scope and Reliability of the Data

This snapshot pulls from the major online operators handling about 70% of the UK's slots market, ensuring robust coverage without capturing every niche player; the Gambling business data on gambling to December 2025, published in February 2026, provides the backbone for these insights, allowing stakeholders to gauge industry health amid ongoing reforms.

Researchers emphasize the data's value for trend-spotting, noting how quarterly comparisons reveal consistencies like the unbroken string of GGY and spin records; it's noteworthy that while GGY rose 10%, outstripping the 7% spin growth, average bet sizes likely held or edged up within limits, sustaining revenue streams.

Yet, as of March 2026, those who've tracked these reports know gaps exist for smaller operators or non-reporting segments, but the 70% representation offers a solid proxy for market-wide dynamics.

Implications for Operators and Regulators

For operators, these numbers affirm adaptability, with spins surging to 25.7 billion and accounts to 4.6 million despite session shortenings; the 10% GGY lift to £788 million signals profitability endures, prompting questions on how game designs evolve to maximize engagement under constraints.

Regulators at the Commission, through releases like this one, highlight successes in curbing long sessions—down 16%—while watching aggregate activity; experts observe that third-quarter peaks post-limits challenge assumptions of sharp downturns, instead showing a market that bends but doesn't break.

One case from earlier quarters involved operators ramping up low-stake, high-volume titles, a tactic seemingly paying off here; it's not rocket science, but the data proves players respond, keeping active numbers climbing even as play times contract.

Conclusion

The UK Gambling Commission's Q3 2025/26 data, fresh from February 2026 analysis, captures online slots at £788 million GGY with 25.7 billion spins, active accounts at 4.6 million, yet shorter 16-minute sessions and fewer hour-plus marathons at 8.9 million; this third consecutive peak since stake limits underscores a resilient sector adapting swiftly, balancing growth with behavioral safeguards across 70% of the market.

As March 2026 unfolds, these figures set the stage for Q4 scrutiny, where